Understanding STRC: How Strategy turns yield demand into BTC buying

Understanding the mechanics, scaling potential, and risks of Strategy’s most important preferred share

Welcome to a new article about MSTR, I’m Viktor and you can find me here on Twitter and here on Telegram. Enjoy your reading !

NB: You can now become a paid subscriber and get access to a growing library of trading resources including monthly recaps of the best trades, links to all my up-to-date TradingView watchlists, actionable trading articles, etc.

We’ve seen a significant increase in $STRC trading volume over the past two weeks, as well as growing interest in this product on CT, so I figured it was a good time to write a new article on Strategy and its new structure.

This is now going to be the fourth article I’ve written about MSTR and the Bitcoin Treasury model:

The first one was an introduction to the MSTR playbook, where I addressed several misconceptions about it.

The second one explained the “full-stack treasury company” model and the mechanism that justifies the premium to NAV (mNAV > 1x).

The third one was an introduction to the Preferred Share Playbook, which is Strategy’s new (and current) model launched in 2025.

In this article, we are going to focus on $STRC, Stretch, which has now become MSTR’s main preferred share as well as the main focus of Saylor and the management team.

What is STRC and how does it work?

First, let me remind you what preferred shares are: to keep it simple, they are debt-like instruments, but they are ultimately equity of the company. This means that these preferred shares never have to be ‘paid back’, and Strategy can’t default on them. Preferred shares sit higher in the capital stack than the common stock $MSTR, meaning that in the case of bankruptcy, preferred shareholders get paid before common shareholders.

So far, Strategy has already issued five preferred shares ($STRF, $STRC, $STRK, $STRE, $STRD), which I introduced one by one in this article. Here are the defining features of $STRC, also called Stretch:

It belongs to the category of “short-duration high-yield credit.”

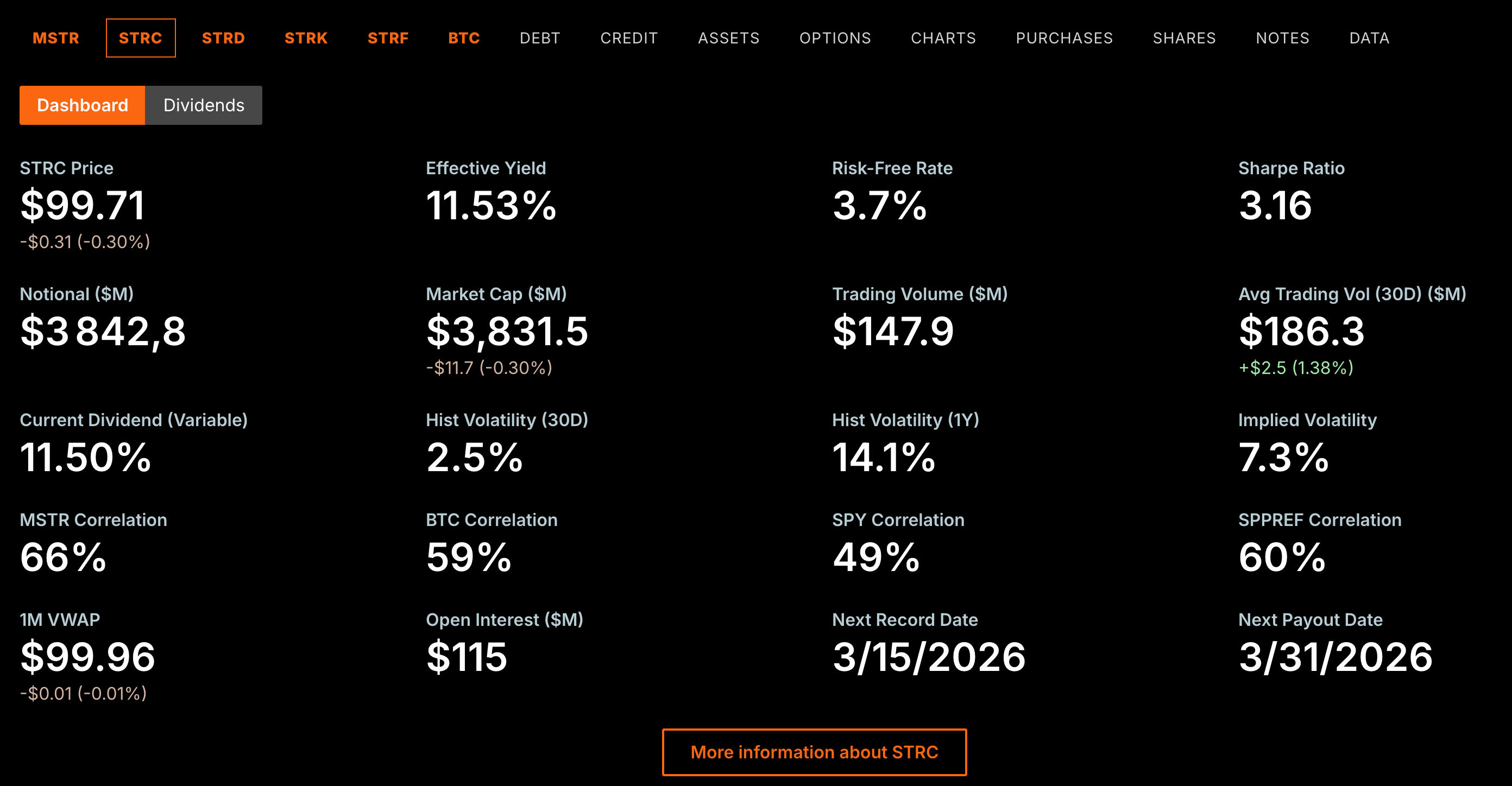

Strategy’s goal is to keep $STRC as close as possible to $100 (”par”), ideally within a 1% range between $99 and $100.

$STRC pays a variable monthly dividend; the current rate is 11.5%.

If $STRC trades too far below par, Strategy can increase the monthly dividend rate so the product becomes more attractive and demand rises until the price moves back toward par.

If $STRC trades above $100, Saylor can issue and sell new $STRC shares at $100 through an ATM (“at-the-market”) program1. This effectively creates a ceiling around $100.

If Saylor doesn’t want to issue shares through the ATM, there is another option: the company can redeem STRC at $101, implying there should be little incentive to buy it above that level.

STRC is a perpetual preferred stock (like every other Strategy preferred), meaning it never comes due and has no maturity date.

How Strategy uses the ATM to control leverage

Even if it’s not strictly debt, Strategy’s preferred shares can be seen as a way to introduce leverage into the balance sheet. Strategy makes a distinction between the leverage ratio (only considering convertible debt against their BTC reserve) and the amplification ratio (convertible debt + preferred shares / BTC reserve), but the amplification ratio is the real way to gauge MSTR’s leverage2.

This means that each time Saylor issues and sells additional STRC shares, he is increasing Strategy’s leverage. The tool he can use to de-lever the company is the ATM on the common stock: by issuing new MSTR shares and buying BTC with the proceeds, he decreases Strategy’s leverage ratio while scaling the company at the same time.

It’s very easy to understand: let’s say a company holds $10bn worth of BTC, has $3bn of debt, and a market cap of $12bn. That would mean that its leverage ratio is $3bn debt / $10bn BTC = 30%.

Now let’s imagine that the company issues $2bn worth of additional shares and then buys $2bn worth of BTC with that money. If we assume that prices don’t move3, then the market cap of the company is now $14bn, and its BTC treasury is now worth $12bn. But the notional amount of debt hasn’t changed, so the new leverage ratio is $3bn debt / $12bn BTC = 25%.

As you can see from this example, using the ATM on the common stock scales the company ($12bn → $14bn market cap) while also reducing its leverage (30% → 25%).

So what is going on with STRC right now? Is Saylor buying a ton of $BTC?

How STRC demand turns into BTC buying:

As I said before, Saylor is a seller of STRC at $100, but not anywhere below $100. This means that whenever the price is trading strictly below $100, all the volume corresponds to STRC shares changing hands between past, present and new holders. And whenever the price is at $100, a portion of the volume corresponds to standard STRC shares changing hands (some people are sellers at $100 too), but the remainder corresponds to Saylor issuing new shares and selling them to the “surplus demand” at $100.

Last week, the ratio between the weekly volume of STRC and the size of the ATM for the week was roughly 40%. I’m going to use this number for the example, but it’s obviously not a rule; it could very well be 25% or 60% in some cases.

This is what happens when $STRC has a $100M volume day while trading at par: Saylor can issue 40% of that amount through the STRC ATM by selling $40M of additional STRC shares. Then he turns around and immediately buys $40M worth of BTC.

But selling STRC (which is a debt-like instrument) increases the leverage of the company, and he wants it to remain stable. Right now, the leverage ratio of MSTR is around 33%, and I think he wants to keep it around this level. This means that each additional dollar of debt must be matched with three dollars of BTC added to the treasury. In our situation, if Saylor adds $40M of debt through STRC and $40M of BTC, then he still needs to add $80M of BTC to the company’s reserves.

How will he do that? By using the ATM on the common stock MSTR, as I explained above. So he’ll issue and sell $80M of new MSTR shares, and then immediately buy $80M worth of BTC with the proceeds.

Conclusion: with this rough math, $100M of daily volume on STRC results in roughly $40M of new STRC issued and $120M of BTC purchased and added to the company’s treasury. With STRC, Strategy has found a way to transform the demand for stable yield into buy pressure for BTC.

What Happens If STRC Demand Explodes? Is Saylor forced to lever to the tits?

Another important thing I want you to notice here is that with the model I just outlined, Strategy could very well multiply the market cap of $STRC by 3x (or, in other words, add $8bn worth of debt through STRC to its current $4bn market cap) without increasing its leverage ratio (i.e., credit risk) at all.

Saylor already has all the tools he needs to increase STRC to whatever size is required to meet the growing demand for this product, while keeping the leverage ratio completely stable at 33%.

Obviously he would increase the notional amount of the company’s debt and the dividend payments he has to make, but it would all scale at the same pace as the BTC treasury, meaning the company wouldn’t be taking any additional risk with respect to BTC price.

What are the real constraints on this strategy?

The mechanism I described above of running both an ATM on STRC and on MSTR at the same time requires two conditions to be met:

The first one is obviously that $STRC must trade at $100: whenever this happens, it simply means that there is more demand for STRC than its current market cap, so Saylor issues new shares to match the surplus demand.

The second one, which I have not mentioned yet, is that the mNAV must be higher than 1x to use the ATM on the common stock. As I explained in detail in this article, the North Star of Strategy is always to increase the bitcoin-per-share (bps) ratio in the long run. When they sell MSTR to buy BTC at an mNAV higher than 1x (i.e., at a premium to NAV), it is accretive in terms of bps. The higher the mNAV, the more accretive it is to do so, and at exactly 1x it is neutral. But when the mNAV drops below 1x, selling MSTR for BTC becomes dilutive in terms of bps, so they will avoid doing it.

As you might have noticed, I mentioned in the previous section that using the ATM on MSTR can scale the company and reduce leverage, but if the mNAV is higher than 1x, then using the ATM on the common stock also has the benefit of increasing the bps ratio.

By the way, the mNAV is literally displayed on the homepage of Strategy.com. They use the most diluted mNAV as their reference (which is the correct thing to do). It is currently at 1.2x, and I think the lowest it has been so far in 2026 is 1x.

What would happen if Saylor had to issue new STRC shares (because of too much demand for STRC) but the mNAV was below 1x? Would that mean he would not be able to use the ATM on MSTR to keep the leverage ratio stable, and would be forced to increase leverage?

Well, first, I think this scenario is rather unlikely, because STRC trading at $100 implies that investors are confident in the overall structure, so MSTR should at least be above 1x mNAV at the same time. And second, this ignores the fact that they have another tool to contain demand for STRC: reducing the dividend rate.

Let’s talk about the dividend rate. “Paying a 11.5% yield doesn’t sound very sustainable.”

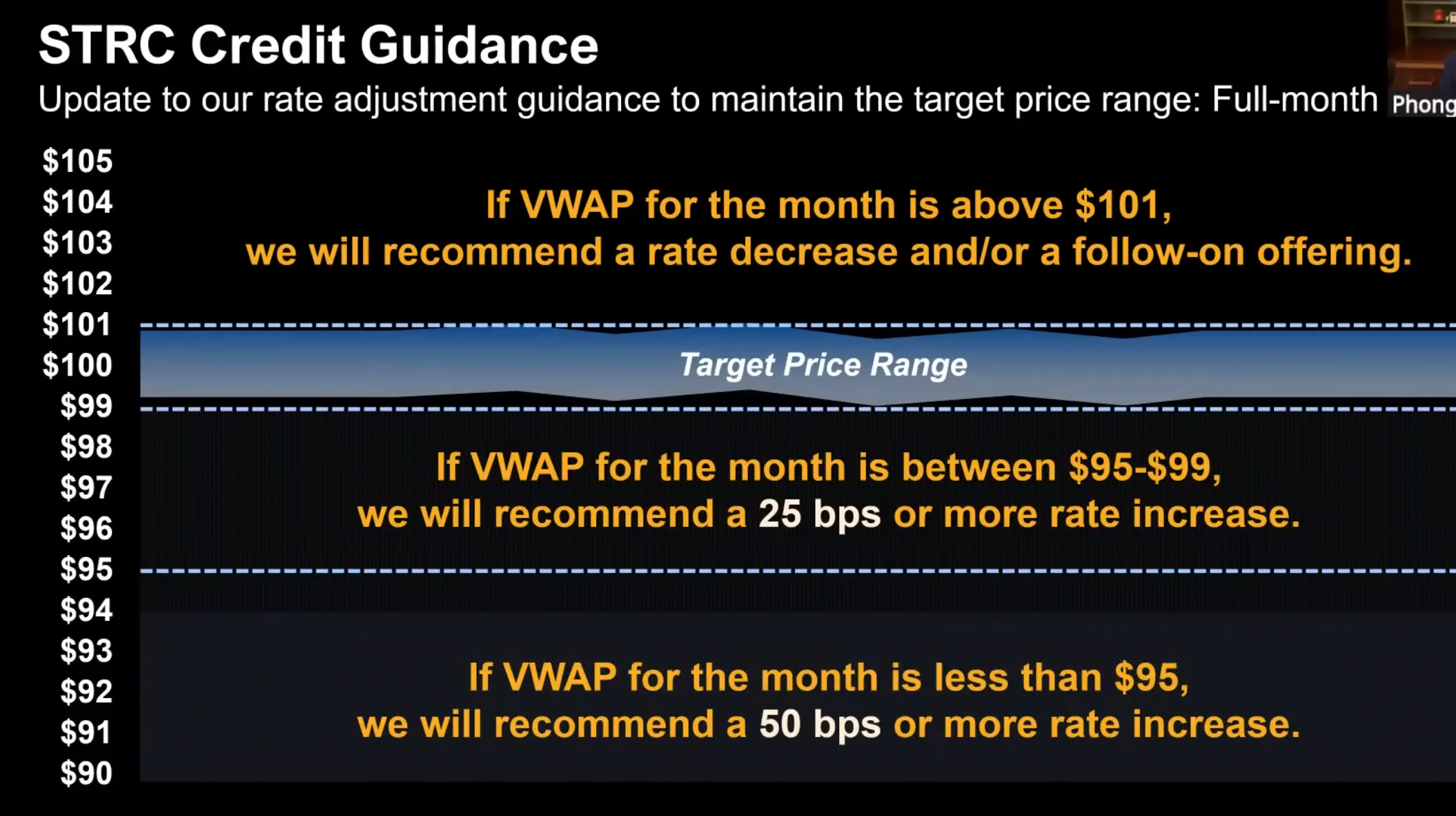

First, let me remind you that STRC launched with a 9% dividend rate. The dividend rate is the tool that can be adjusted to both match demand for STRC and ensure that it trades at par. The current guidance from Strategy is that they will increase the dividend rate by 25 bps if the monthly VWAP (on STRC) is between $95 and $99, and they will increase it by 50 bps if the monthly VWAP is below $95. They will also decrease the dividend rate if the monthly VWAP is above $101.

So basically what they have done so far is progressively increase the STRC dividend rate from 9% to 11.5% in order to reach an equilibrium where STRC trades around $100 on a daily basis. The current week has been the most successful week for STRC by far, because it has not only been trading consistently at par, but also with huge volume (around $300M–$400M a day, compared to slightly more than $100M on average).

The demand for STRC fundamentally depends on a few variables:

Credit risk: What is the current leverage ratio of Strategy, or in other words, how much BTC is currently ‘backing’ STRC? This is a direct consequence of the BTC price: if BTC goes down, all else being equal, the leverage ratio goes up, the credit risk increases, and demand for STRC should decline (i.e., STRC price down).

Yield: What dividend rate is STRC currently paying? The higher the dividend rate, the higher the demand for STRC.

Awareness: How many people even know about STRC? This is a very important factor during the first months or years of the product, because it is basically a variable that can only go up, and it can significantly affect demand for STRC, all else being equal.

Confidence: How many people feel comfortable putting their money in STRC after seeing it trade for months and consistently pay dividends? This is a special factor because confidence can vary a lot: if STRC trades in a very narrow range close to $100 for a long time, more and more people will consider it safe, but if we suddenly see a 10% dip in one day, that trust can evaporate quickly.

What we’ve seen so far since inception is that credit risk has gone up (because of the 45% drop in BTC from its ATH), the yield has gone up, awareness has gone up, and confidence has gone up too. One factor has impacted demand negatively, while the three others have impacted it positively, and we are now finally in the “ideal” situation where STRC remains at $100.

An 11.5% yield was the dividend rate required to bring STRC to par with BTC trading around $68k. This sounds quite constructive to me for a product that has been trading for less than eight months. Saylor expects BTC to grow at a 20-30% CAGR over the next 20 years. As I explained in detail here, under these assumptions, issuing debt at 11.5% interest to buy an asset growing at 25% per year makes perfect sense. In theory, you could even pay a higher interest rate and still make money by arbitraging the spread between the interest paid and BTC’s expected annual return.

The most likely path in my view is that demand for STRC will continue to grow, and Strategy will progressively decrease the dividend rate back to 10% (or even below in the long run) to contain demand while reducing their interest cost.

What happens if everyone tries to exit STRC?

Well, the price of STRC will dump in this situation! But that’s exactly what we’ve already seen a few times with this product: in August 2025, it dumped 6% from $98 to $92; during the November 2025 sell-off, STRC dumped 11% from $100 to $89; and in February, it dumped 7% from $100 to $93.

You have to be aware that Saylor’s stated goal is clearly for $STRC to remain in a tight range close to $100, and STRC has become the main focus of Strategy. So if STRC trades on average below $99 over the course of a month, Strategy will increase the dividend rate to bring demand back in line with a $100 price. As long as people are confident in Strategy’s ability to maintain this, there will always be dip buyers below $100 looking to play the “arb trade” back to par.

In the short term, the price can very well dip 10% because of panic among holders, but if you are confident in the structure put in place by Strategy, then the price should move back to par within a few days or a few weeks, as we’ve already seen in the past.

What prevents the dividend from just rising forever?

Let’s imagine that STRC doesn’t go back to par. That would mean Strategy has to keep increasing the dividend rate… and since there is no formal limit to how high it can go, this might start to look like a death-spiral scenario? Well, not exactly.

First, you have to understand that the dividend “guidance” does not legally bind Saylor to do anything. At the end of the day, the company is free to do whatever it wants with respect to the dividend rate, and it can stop increasing it even if the average price for the month is below $99.

Basically, if they expect BTC to grow at 20–30% per year, then they probably have in mind a “maximum” dividend rate they would be comfortable paying, maybe something like 15%. Once that level is reached, they could simply stop increasing the dividend regardless of where STRC is trading.

Keep in mind that the dividend rate can be adjusted monthly, and if you expect BTC to recover after a bear market, then a “high dividend rate” would not need to be maintained forever. As the price of BTC rises again, the credit risk of STRC would improve, which would mechanically increase demand for STRC and bring it back toward par. At that point, the company could start reducing the dividend rate again. Over the long run, the dividend rate of STRC could very well fall to something like 8%, even if it had temporarily reached 13% during a period of stress.

In the next section (Risk #4 below), I will outline what a worst-case scenario might look like if BTC enters a prolonged bear market and Saylor is forced to keep raising the dividend rate.

Understanding the Risks

This whole article sounds like nothing can go wrong, and I don’t believe in a free lunch at all. What are the actual risks I’m taking as a STRC holder?

Let me be very clear about my stance on this matter: I think the risk of STRC is mispriced right now, and that the yield-to-risk ratio is attractive given reasonably bullish assumptions for BTC price. But I am NOT saying that you can get paid a high yield with no risk. There is risk, and it is always tied to BTC performance.

But I think there is a mismatch between what price trajectory people expect for BTC and the perceived risk of STRC. Basically, I think that if you take crypto natives’ expectations for BTC over the coming years, 95% of them expect a scenario that would leave STRC largely unaffected, meaning they could clip a 10%+ yield with “low risk” according to their own BTC expectations. But let’s talk about the risks.

Risk #1: Asymmetric downside vs upside

The structure of STRC means that if you buy it at $100, your upside is capped at the yearly dividend payments (11.5% right now), while your downside can be anywhere between 0 and 10% in just a few days, based on historical price action. This means that if STRC dumps 6% in a week, you have temporarily lost the equivalent of half a year’s worth of dividends, which can be a problem if you need to exit your position quickly.

If your goal is to hold STRC for the long term, it doesn’t really matter because if you’re confident it will always get back to $100, then you’ll eventually be able to exit your position with no haircut. (Let me remind you that the return-of-capital nature of STRC dividends means holders are incentivized not to trade it short term, since they don’t have to pay taxes on the dividends.)

Risk #2: STRC dumps at the same time as BTC

The credit risk of STRC is directly related to the price of BTC, so as you have probably noticed, the drawdowns in STRC tend to happen at the same time as the largest sell-offs in BTC. This means your “stable”, yield-generating allocation can take a haircut precisely when you are already most vulnerable as a crypto bull.

Risk #3: STRC trades at a discount for an extended period of time

The trust people have in STRC’s ability to return to par comes from both its actual credit risk and the perceived risk inferred from historical price action. This second factor could work in reverse: if everyone expects a 5% dip to get bought back up but it doesn’t, what happens?

Then the people who bought the 5% dip exit their positions and the price drops further, potentially triggering additional emotional selling levels one by one, resulting in an even larger drawdown. If we imagine a scenario where STRC is down 15% and unable to bounce back for several days, then the confidence accumulated in the product could progressively erode, triggering even more selling pressure.

What can stop the vicious cycle in that situation? As always, it’s the price of BTC that would resolve it. Saylor’s entire strategy ultimately relies on the expectation that BTC will return 20%+ annually over the next decade or more.

What would the worst-case scenario look like?

Risk #4: the fundamental risk is always BTC performance

The worst-case scenario for STRC is the one I described just above, but with BTC being unable to regain strength during a prolonged bear market. It’s obviously very hard to have a clear vision of what would happen in this situation because of how many variables are involved, but it would look something like this:

$STRC would trade below par, so Saylor would increase the dividend rate every month to try to bring it back to $100.

At some point, the dividend rate would become too elevated to make sense, so he would keep it stable and stop increasing it. That would mean he would stop following his “guidance” of increasing the dividend rate when the monthly VWAP is below $99. Remember that this is only guidance, nothing forces him to follow it.

Not following the guidance would hurt confidence in STRC even more, and it could continue trading at a large discount, maybe something like a 40% discount and a 15% dividend rate, implying an effective yield of 25%.

$MSTR would trade below 1x mNAV, meaning they wouldn’t be able to sell MSTR shares to help cover the dividends.

Strategy would then rely entirely on its USD reserves to pay the dividends, and currently they have 28 months (2 years and 4 months) worth of dividend payments in reserve.

As we approach the end of those 28 months, all of the instruments would likely face even more pressure: BTC, MSTR, and STRC would have even more reasons to decline.

Once the USD reserve is depleted, Strategy would have to sell BTC gradually. Right now the yearly dividends are around $1bn, so if that were to increase to $2bn, Strategy would have to sell about $200M worth of BTC each month to keep paying the dividends. Alternatively, they could decide to stop paying the dividends, in which case the value of the preferred shares, of STRC, and of MSTR would drop even further, and they wouldn’t be able to do much until the price of BTC recovers.

So this is roughly an outline of the worst-case scenario. As you can see, the USD reserve offers a huge buffer against a bearish scenario, because Strategy could theoretically stop doing anything and just keep paying the dividends for more than two years without being forced to act.

Right now we are in the middle of a BTC bear market, with the price around $70k (down about 45% from the top), and yet $STRC is trading at par (with an 11.5% dividend rate) and the mNAV is at 1.2x. Given that I don’t expect BTC to experience a two-year bear market (the 2022 bear market lasted roughly one year from top to bottom), and that Strategy hasn’t even had to start using its USD reserves yet, I am of the opinion that the overall structure of Strategy is quite safe and resilient at the current leverage ratio.

The main risk is… that it’s working too well?

As I tweeted yesterday, I think that as a BTC bull, the main risk related to MSTR is that it works too well.

In fact, MSTR already owns about 3.5% of the total BTC supply, and that could negatively affect future demand for BTC, as it may start to taint the narrative of BTC as a pristine decentralized asset. The “Digital Credit” narrative around STRC and its high yield is also creating a negative reaction among some people in crypto, once again potentially impacting BTC demand as a consequence.

And as I’ve explained throughout this article, the amount of BTC that Strategy holds will only keep increasing. The only scenario where this is not true is one where we get at least two years of pain in BTC. And even then, it would take many more years of bad price action to slowly deplete Strategy’s BTC reserves through dividend payments.

I can understand why some people are bothered by MSTR’s involvement in BTC, but to me, if that is enough to make you flip bearish on the long-term prospects of BTC, then you probably weren’t that bullish to begin with. To me, it isn’t that big of a deal. Sure, Strategy is a single entity holding 3.5% of the BTC supply, but at the end of the day Strategy and its BTC reserves belong to its shareholders.

Is that really so different from BlackRock effectively holding a similar amount on behalf of its IBIT shareholders? They are obviously not the same thing at all, and there is no bankruptcy risk for IBIT, but to me they are somewhat similar: they both represent the financialization of BTC, and they were both inevitable.

I don’t think Strategy and STRC are a systemic risk for BTC at all, but I can see the negative impact they may have on the narrative. Anyway, this article is mostly here to educate people about STRC and the structure of Strategy, after that, you can decide for yourself how bullish or bearish you want to be.

Is STRC a new UST/Anchor?

I think the Luna / UST / Anchor comparison has been mentioned so often on CT lately that it’s worth addressing it. It’s a completely different situation on many levels:

UST was a stablecoin, so maintaining the $1 peg was absolutely critical. STRC is a preferred share that ideally trades within a 1% range close to $100, but it can very well drop several percent below $100. It has already happened, it will happen again, and it is not necessarily a problem.

UST was backed by LUNA, and the value of LUNA was partially tied to the success of UST. When UST traded below peg, users could redeem UST for newly minted LUNA. This increased selling pressure on LUNA, which reduced confidence in the system and created even more selling pressure on UST. The result was a reflexive death spiral that drove both UST and LUNA effectively to zero within days. This kind of reflexive mechanism does not exist with STRC, because a decline in STRC does not trigger forced issuance, redemptions, or dilution elsewhere in the system, it doesn’t affect BTC.

The Anchor yield on UST was 18-20%. Not only was it significantly higher than the current ~11.5% yield on STRC, it was also largely subsidized and structurally unsustainable. The source of the STRC yield is relatively straightforward: Strategy expects BTC to return more than 20% annually over the coming decade. STRC holders receive the first ~11.5% (or whatever the dividend rate is at the time) with relatively low volatility, while MSTR shareholders absorb the remaining upside and volatility.

We know exactly how Strategy can keep paying the dividend. If mNAV is above 1x, they can sell MSTR shares through the ATM. If mNAV drops below 1x, they can rely on the USD reserve (which currently covers more than two years of dividends). If the reserve were depleted, they could ultimately sell BTC derivatives or BTC from their treasury. With UST and Anchor, it was just “trust me bro, we’ll keep paying”.

A drop in price affects the two systems very differently. When UST lost its peg, confidence collapsed and the market quickly assumed the system could go to zero. With STRC, a lower price mechanically implies a higher effective yield, which can attract new buyers. For example, in a completely bearish scenario, if STRC were trading at $50 with a 12% dividend rate, the effective yield would be around 24%.

Finally, the time dynamics are completely different. Luna/UST was a fragile system that could collapse in a matter of days after a loss of confidence. In the case of STRC, even the worst-case scenario outlined earlier would unfold much more slowly (very slow death), potentially over several years, unless you assume a sudden and catastrophic collapse (-90%) in the price of BTC in just a few months.

TL;DR

STRC is a yield instrument backed by Strategy’s bitcoin treasury. Its dividend rate is dynamically adjusted to keep the price close to par ($100).

You can currently earn an 11.5% annual yield paid monthly on a mostly stable instrument, with very transparent risk.

STRC is essentially a way for Strategy to turn demand for yield into structural buying pressure for BTC.

The structure can scale massively without increasing MSTR’s leverage, as long as Strategy simultaneously runs ATMs on both STRC and MSTR (mNAV>1x required). This means Strategy could absorb $10bn (or much more) of new demand into STRC while keeping its leverage ratio stable at around 33% and its credit risk unchanged.

Every $1 of STRC issued should roughly translate into $3 of BTC added to the treasury, thanks to the common-stock ATM used to maintain the leverage ratio. Based on rough math, $100M of daily STRC volume at par ($100) can lead to $100M-$150M of BTC purchase.

Strategy effectively turns BTC exposure into two different tranches of risk: STRC holders receive a relatively stable yield with low volatility, while MSTR shareholders absorb the remaining upside and volatility of BTC. As Lavoisier famously put it: “Nothing is lost, nothing is created, everything is transformed.”

The whole structure is designed to increase bitcoin-per-share (bps) over time, which ultimately benefits MSTR common shareholders, because it means MSTR should mechanically outperform BTC.

Short-term drawdowns of 5-10% in STRC are possible, but as long as confidence in the structure remains intact, the market tends to arbitrage the price back toward par.

The real risk is not a sudden collapse but a prolonged BTC bear market, which could gradually stress the structure over time.

Even the (very unlikely) worst-case scenario would unfold slowly, thanks to the USD reserve and the flexibility Strategy has to adjust the dividend. If MSTR were to collapse, it would likely not happen in a spectacular and brutal way like Luna/UST, but rather through a slow and prolonged deterioration.

It makes very little sense to be bullish on BTC while being bearish on MSTR and STRC. Based on Strategy’s current level of risk (subject to change), MSTR can’t really die without BTC dying first.

I hope this article makes a few things clearer about STRC and the current MSTR playbook. If you have any questions or would like me to clarify something, feel free to comment below or ask me directly on Twitter!

ATM = “At-the-Market” program, allowing a company to issue and sell shares directly into the market at the prevailing price.

So I’m going to say ‘leverage’ even if I’m referring to the amplification ratio.

In practice, prices would obviously be affected, but given that the company’s stock price and BTC price are highly correlated, it’s a reasonable simplifying assumption

’ve seen a significant increase in $STRC trading volume over the past two weeks, as well as growing interest in this product on CT, so I figured it was a good time to write a new article on Strategy and its new structure.

This is now going to be the fourth article I’ve written about MSTR and the Bitcoin Treasury model:

The first one was an introduction to the MSTR playbook, where I addressed several misconceptions about it.

The second one explained the “full-stack treasury company” model and the mechanism that justifies the premium to NAV (mNAV > 1x).

The third one was an introduction to the Preferred Share Playbook, which is Strategy’s new (and current) model launched in 2025.

In this article, we are going to focus on $STRC, Stretch, which has now become MSTR’s main preferred share as well as the main focus of Saylor and the management team.

What is STRC and how does it work?

First, let me remind you what preferred shares are: to keep it simple, they are debt-like instruments, but they are ultimately equity of the company. This means that these preferred shares never have to be ‘paid back’, and Strategy can’t default on them. Preferred shares sit higher in the capital stack than the common stock $MSTR, meaning that in the case of bankruptcy, preferred shareholders get paid before common shareholders.

So far, Strategy has already issued five preferred shares ($STRF, $STRC, $STRK, $STRE, $STRD), which I introduced one by one in this article. Here are the defining features of $STRC, also called Stretch:

It belongs to the category of “short-duration high-yield credit.”

Strategy’s goal is to keep $STRC as close as possible to $100 (”par”), ideally within a 1% range between $99 and $100.

$STRC pays a variable monthly dividend; the current rate is 11.5%.

If $STRC trades too far below par, Strategy can increase the monthly dividend rate so the product becomes more attractive and demand rises until the price moves back toward par.

If $STRC trades above $100, Saylor can issue and sell new $STRC shares at $100 through an ATM (“at-the-market”) program1. This effectively creates a ceiling around $100.

If Saylor doesn’t want to issue shares through the ATM, there is another option: the company can redeem STRC at $101, implying there should be little incentive to buy it above that level.

STRC is a perpetual preferred stock (like every other Strategy preferred), meaning it never comes due and has no maturity date.

How Strategy uses the ATM to control leverage

Even if it’s not strictly debt, Strategy’s preferred shares can be seen as a way to introduce leverage into the balance sheet. Strategy makes a distinction between the leverage ratio (only considering convertible debt against their BTC reserve) and the amplification ratio (convertible debt + preferred shares / BTC reserve), but the amplification ratio is the real way to gauge MSTR’s leverage2.

This means that each time Saylor issues and sells additional STRC shares, he is increasing Strategy’s leverage. The tool he can use to de-lever the company is the ATM on the common stock: by issuing new MSTR shares and buying BTC with the proceeds, he decreases Strategy’s leverage ratio while scaling the company at the same time.

It’s very easy to understand: let’s say a company holds $10bn worth of BTC, has $3bn of debt, and a market cap of $12bn. That would mean that its leverage ratio is $3bn debt / $10bn BTC = 30%.

Now let’s imagine that the company issues $2bn worth of additional shares and then buys $2bn worth of BTC with that money. If we assume that prices don’t move3, then the market cap of the company is now $14bn, and its BTC treasury is now worth $12bn. But the notional amount of debt hasn’t changed, so the new leverage ratio is $3bn debt / $12bn BTC = 25%.

As you can see from this example, using the ATM on the common stock scales the company ($12bn → $14bn market cap) while also reducing its leverage (30% → 25%).

So what is going on with STRC right now? Is Saylor buying a ton of $BTC?

How STRC demand turns into BTC buying:

As I said before, Saylor is a seller of STRC at $100, but not anywhere below $100. This means that whenever the price is trading strictly below $100, all the volume corresponds to STRC shares changing hands between past, present and new holders. And whenever the price is at $100, a portion of the volume corresponds to standard STRC shares changing hands (some people are sellers at $100 too), but the remainder corresponds to Saylor issuing new shares and selling them to the “surplus demand” at $100.

Last week, the ratio between the weekly volume of STRC and the size of the ATM for the week was roughly 40%. I’m going to use this number for the example, but it’s obviously not a rule; it could very well be 25% or 60% in some cases.

This is what happens when $STRC has a $100M volume day while trading at par: Saylor can issue 40% of that amount through the STRC ATM by selling $40M of additional STRC shares. Then he turns around and immediately buys $40M worth of BTC.

But selling STRC (which is a debt-like instrument) increases the leverage of the company, and he wants it to remain stable. Right now, the leverage ratio of MSTR is around 33%, and I think he wants to keep it around this level. This means that each additional dollar of debt must be matched with three dollars of BTC added to the treasury. In our situation, if Saylor adds $40M of debt through STRC and $40M of BTC, then he still needs to add $80M of BTC to the company’s reserves.

How will he do that? By using the ATM on the common stock MSTR, as I explained above. So he’ll issue and sell $80M of new MSTR shares, and then immediately buy $80M worth of BTC with the proceeds.

Conclusion: with this rough math, $100M of daily volume on STRC results in roughly $40M of new STRC issued and $120M of BTC purchased and added to the company’s treasury. With STRC, Strategy has found a way to transform the demand for stable yield into buy pressure for BTC.

What Happens If STRC Demand Explodes? Is Saylor forced to lever to the tits?

Another important thing I want you to notice here is that with the model I just outlined, Strategy could very well multiply the market cap of $STRC by 3x (or, in other words, add $8bn worth of debt through STRC to its current $4bn market cap) without increasing its leverage ratio (i.e., credit risk) at all.

Saylor already has all the tools he needs to increase STRC to whatever size is required to meet the growing demand for this product, while keeping the leverage ratio completely stable at 33%.

Obviously he would increase the notional amount of the company’s debt and the dividend payments he has to make, but it would all scale at the same pace as the BTC treasury, meaning the company wouldn’t be taking any additional risk with respect to BTC price.

What are the real constraints on this strategy?

The mechanism I described above of running both an ATM on STRC and on MSTR at the same time requires two conditions to be met:

The first one is obviously that $STRC must trade at $100: whenever this happens, it simply means that there is more demand for STRC than its current market cap, so Saylor issues new shares to match the surplus demand.

The second one, which I have not mentioned yet, is that the mNAV must be higher than 1x to use the ATM on the common stock. As I explained in detail in this article, the North Star of Strategy is always to increase the bitcoin-per-share (bps) ratio in the long run. When they sell MSTR to buy BTC at an mNAV higher than 1x (i.e., at a premium to NAV), it is accretive in terms of bps. The higher the mNAV, the more accretive it is to do so, and at exactly 1x it is neutral. But when the mNAV drops below 1x, selling MSTR for BTC becomes dilutive in terms of bps, so they will avoid doing it.

As you might have noticed, I mentioned in the previous section that using the ATM on MSTR can scale the company and reduce leverage, but if the mNAV is higher than 1x, then using the ATM on the common stock also has the benefit of increasing the bps ratio.

By the way, the mNAV is literally displayed on the homepage of Strategy.com. They use the most diluted mNAV as their reference (which is the correct thing to do). It is currently at 1.2x, and I think the lowest it has been so far in 2026 is 1x.

What would happen if Saylor had to issue new STRC shares (because of too much demand for STRC) but the mNAV was below 1x? Would that mean he would not be able to use the ATM on MSTR to keep the leverage ratio stable, and would be forced to increase leverage?

Well, first, I think this scenario is rather unlikely, because STRC trading at $100 implies that investors are confident in the overall structure, so MSTR should at least be above 1x mNAV at the same time. And second, this ignores the fact that they have another tool to contain demand for STRC: reducing the dividend rate.

Let’s talk about the dividend rate. “Paying a 11.5% yield doesn’t sound very sustainable.”

First, let me remind you that STRC launched with a 9% dividend rate. The dividend rate is the tool that can be adjusted to both match demand for STRC and ensure that it trades at par. The current guidance from Strategy is that they will increase the dividend rate by 25 bps if the monthly VWAP (on STRC) is between $95 and $99, and they will increase it by 50 bps if the monthly VWAP is below $95. They will also decrease the dividend rate if the monthly VWAP is above $101.

So basically what they have done so far is progressively increase the STRC dividend rate from 9% to 11.5% in order to reach an equilibrium where STRC trades around $100 on a daily basis. The current week has been the most successful week for STRC by far, because it has not only been trading consistently at par, but also with huge volume (around $300M–$400M a day, compared to slightly more than $100M on average).

The demand for STRC fundamentally depends on a few variables:

Credit risk: What is the current leverage ratio of Strategy, or in other words, how much BTC is currently ‘backing’ STRC? This is a direct consequence of the BTC price: if BTC goes down, all else being equal, the leverage ratio goes up, the credit risk increases, and demand for STRC should decline (i.e., STRC price down).

Yield: What dividend rate is STRC currently paying? The higher the dividend rate, the higher the demand for STRC.

Awareness: How many people even know about STRC? This is a very important factor during the first months or years of the product, because it is basically a variable that can only go up, and it can significantly affect demand for STRC, all else being equal.

Confidence: How many people feel comfortable putting their money in STRC after seeing it trade for months and consistently pay dividends? This is a special factor because confidence can vary a lot: if STRC trades in a very narrow range close to $100 for a long time, more and more people will consider it safe, but if we suddenly see a 10% dip in one day, that trust can evaporate quickly.

What we’ve seen so far since inception is that credit risk has gone up (because of the 45% drop in BTC from its ATH), the yield has gone up, awareness has gone up, and confidence has gone up too. One factor has impacted demand negatively, while the three others have impacted it positively, and we are now finally in the “ideal” situation where STRC remains at $100.

An 11.5% yield was the dividend rate required to bring STRC to par with BTC trading around $68k. This sounds quite constructive to me for a product that has been trading for less than eight months. Saylor expects BTC to grow at a 20-30% CAGR over the next 20 years. As I explained in detail here, under these assumptions, issuing debt at 11.5% interest to buy an asset growing at 25% per year makes perfect sense. In theory, you could even pay a higher interest rate and still make money by arbitraging the spread between the interest paid and BTC’s expected annual return.

The most likely path in my view is that demand for STRC will continue to grow, and Strategy will progressively decrease the dividend rate back to 10% (or even below in the long run) to contain demand while reducing their interest cost.

What happens if everyone tries to exit STRC?

Well, the price of STRC will dump in this situation! But that’s exactly what we’ve already seen a few times with this product: in August 2025, it dumped 6% from $98 to $92; during the November 2025 sell-off, STRC dumped 11% from $100 to $89; and in February, it dumped 7% from $100 to $93.

You have to be aware that Saylor’s stated goal is clearly for $STRC to remain in a tight range close to $100, and STRC has become the main focus of Strategy. So if STRC trades on average below $99 over the course of a month, Strategy will increase the dividend rate to bring demand back in line with a $100 price. As long as people are confident in Strategy’s ability to maintain this, there will always be dip buyers below $100 looking to play the “arb trade” back to par.

In the short term, the price can very well dip 10% because of panic among holders, but if you are confident in the structure put in place by Strategy, then the price should move back to par within a few days or a few weeks, as we’ve already seen in the past.

What prevents the dividend from just rising forever?

Let’s imagine that STRC doesn’t go back to par. That would mean Strategy has to keep increasing the dividend rate… and since there is no formal limit to how high it can go, this might start to look like a death-spiral scenario? Well, not exactly.

First, you have to understand that the dividend “guidance” does not legally bind Saylor to do anything. At the end of the day, the company is free to do whatever it wants with respect to the dividend rate, and it can stop increasing it even if the average price for the month is below $99.

Basically, if they expect BTC to grow at 20–30% per year, then they probably have in mind a “maximum” dividend rate they would be comfortable paying, maybe something like 15%. Once that level is reached, they could simply stop increasing the dividend regardless of where STRC is trading.

Keep in mind that the dividend rate can be adjusted monthly, and if you expect BTC to recover after a bear market, then a “high dividend rate” would not need to be maintained forever. As the price of BTC rises again, the credit risk of STRC would improve, which would mechanically increase demand for STRC and bring it back toward par. At that point, the company could start reducing the dividend rate again. Over the long run, the dividend rate of STRC could very well fall to something like 8%, even if it had temporarily reached 13% during a period of stress.

In the next section (Risk #4 below), I will outline what a worst-case scenario might look like if BTC enters a prolonged bear market and Saylor is forced to keep raising the dividend rate.

Understanding the Risks

This whole article sounds like nothing can go wrong, and I don’t believe in a free lunch at all. What are the actual risks I’m taking as a STRC holder?

Let me be very clear about my stance on this matter: I think the risk of STRC is mispriced right now, and that the yield-to-risk ratio is attractive given reasonably bullish assumptions for BTC price. But I am NOT saying that you can get paid a high yield with no risk. There is risk, and it is always tied to BTC performance.

But I think there is a mismatch between what price trajectory people expect for BTC and the perceived risk of STRC. Basically, I think that if you take crypto natives’ expectations for BTC over the coming years, 95% of them expect a scenario that would leave STRC largely unaffected, meaning they could clip a 10%+ yield with “low risk” according to their own BTC expectations. But let’s talk about the risks.

Risk #1: Asymmetric downside vs upside

The structure of STRC means that if you buy it at $100, your upside is capped at the yearly dividend payments (11.5% right now), while your downside can be anywhere between 0 and 10% in just a few days, based on historical price action. This means that if STRC dumps 6% in a week, you have temporarily lost the equivalent of half a year’s worth of dividends, which can be a problem if you need to exit your position quickly.

If your goal is to hold STRC for the long term, it doesn’t really matter because if you’re confident it will always get back to $100, then you’ll eventually be able to exit your position with no haircut. (Let me remind you that the return-of-capital nature of STRC dividends means holders are incentivized not to trade it short term, since they don’t have to pay taxes on the dividends.)

Risk #2: STRC dumps at the same time as BTC

The credit risk of STRC is directly related to the price of BTC, so as you have probably noticed, the drawdowns in STRC tend to happen at the same time as the largest sell-offs in BTC. This means your “stable”, yield-generating allocation can take a haircut precisely when you are already most vulnerable as a crypto bull.

Risk #3: STRC trades at a discount for an extended period of time

The trust people have in STRC’s ability to return to par comes from both its actual credit risk and the perceived risk inferred from historical price action. This second factor could work in reverse: if everyone expects a 5% dip to get bought back up but it doesn’t, what happens?

Then the people who bought the 5% dip exit their positions and the price drops further, potentially triggering additional emotional selling levels one by one, resulting in an even larger drawdown. If we imagine a scenario where STRC is down 15% and unable to bounce back for several days, then the confidence accumulated in the product could progressively erode, triggering even more selling pressure.

What can stop the vicious cycle in that situation? As always, it’s the price of BTC that would resolve it. Saylor’s entire strategy ultimately relies on the expectation that BTC will return 20%+ annually over the next decade or more.

What would the worst-case scenario look like?

Risk #4: the fundamental risk is always BTC performance

The worst-case scenario for STRC is the one I described just above, but with BTC being unable to regain strength during a prolonged bear market. It’s obviously very hard to have a clear vision of what would happen in this situation because of how many variables are involved, but it would look something like this:

$STRC would trade below par, so Saylor would increase the dividend rate every month to try to bring it back to $100.

At some point, the dividend rate would become too elevated to make sense, so he would keep it stable and stop increasing it. That would mean he would stop following his “guidance” of increasing the dividend rate when the monthly VWAP is below $99. Remember that this is only guidance, nothing forces him to follow it.

Not following the guidance would hurt confidence in STRC even more, and it could continue trading at a large discount, maybe something like a 40% discount and a 15% dividend rate, implying an effective yield of 25%.

$MSTR would trade below 1x mNAV, meaning they wouldn’t be able to sell MSTR shares to help cover the dividends.

Strategy would then rely entirely on its USD reserves to pay the dividends, and currently they have 28 months (2 years and 4 months) worth of dividend payments in reserve.

As we approach the end of those 28 months, all of the instruments would likely face even more pressure: BTC, MSTR, and STRC would have even more reasons to decline.

Once the USD reserve is depleted, Strategy would have to sell BTC gradually. Right now the yearly dividends are around $1bn, so if that were to increase to $2bn, Strategy would have to sell about $200M worth of BTC each month to keep paying the dividends. Alternatively, they could decide to stop paying the dividends, in which case the value of the preferred shares, of STRC, and of MSTR would drop even further, and they wouldn’t be able to do much until the price of BTC recovers.

So this is roughly an outline of the worst-case scenario. As you can see, the USD reserve offers a huge buffer against a bearish scenario, because Strategy could theoretically stop doing anything and just keep paying the dividends for more than two years without being forced to act.

Right now we are in the middle of a BTC bear market, with the price around $70k (down about 45% from the top), and yet $STRC is trading at par (with an 11.5% dividend rate) and the mNAV is at 1.2x. Given that I don’t expect BTC to experience a two-year bear market (the 2022 bear market lasted roughly one year from top to bottom), and that Strategy hasn’t even had to start using its USD reserves yet, I am of the opinion that the overall structure of Strategy is quite safe and resilient at the current leverage ratio.

The main risk is… that it’s working too well?

As I tweeted yesterday, I think that as a BTC bull, the main risk related to MSTR is that it works too well.

In fact, MSTR already owns about 3.5% of the total BTC supply, and that could negatively affect future demand for BTC, as it may start to taint the narrative of BTC as a pristine decentralized asset. The “Digital Credit” narrative around STRC and its high yield is also creating a negative reaction among some people in crypto, once again potentially impacting BTC demand as a consequence.

And as I’ve explained throughout this article, the amount of BTC that Strategy holds will only keep increasing. The only scenario where this is not true is one where we get at least two years of pain in BTC. And even then, it would take many more years of bad price action to slowly deplete Strategy’s BTC reserves through dividend payments.

I can understand why some people are bothered by MSTR’s involvement in BTC, but to me, if that is enough to make you flip bearish on the long-term prospects of BTC, then you probably weren’t that bullish to begin with. To me, it isn’t that big of a deal. Sure, Strategy is a single entity holding 3.5% of the BTC supply, but at the end of the day Strategy and its BTC reserves belong to its shareholders.

Is that really so different from BlackRock effectively holding a similar amount on behalf of its IBIT shareholders? They are obviously not the same thing at all, and there is no bankruptcy risk for IBIT, but to me they are somewhat similar: they both represent the financialization of BTC, and they were both inevitable.

I don’t think Strategy and STRC are a systemic risk for BTC at all, but I can see the negative impact they may have on the narrative. Anyway, this article is mostly here to educate people about STRC and the structure of Strategy, after that, you can decide for yourself how bullish or bearish you want to be.

Is STRC a new UST/Anchor?

I think the Luna / UST / Anchor comparison has been mentioned so often on CT lately that it’s worth addressing it. It’s a completely different situation on many levels:

UST was a stablecoin, so maintaining the $1 peg was absolutely critical. STRC is a preferred share that ideally trades within a 1% range close to $100, but it can very well drop several percent below $100. It has already happened, it will happen again, and it is not necessarily a problem.

UST was backed by LUNA, and the value of LUNA was partially tied to the success of UST. When UST traded below peg, users could redeem UST for newly minted LUNA. This increased selling pressure on LUNA, which reduced confidence in the system and created even more selling pressure on UST. The result was a reflexive death spiral that drove both UST and LUNA effectively to zero within days. This kind of reflexive mechanism does not exist with STRC, because a decline in STRC does not trigger forced issuance, redemptions, or dilution elsewhere in the system, it doesn’t affect BTC.

The Anchor yield on UST was 18-20%. Not only was it significantly higher than the current ~11.5% yield on STRC, it was also largely subsidized and structurally unsustainable. The source of the STRC yield is relatively straightforward: Strategy expects BTC to return more than 20% annually over the coming decade. STRC holders receive the first ~11.5% (or whatever the dividend rate is at the time) with relatively low volatility, while MSTR shareholders absorb the remaining upside and volatility.

We know exactly how Strategy can keep paying the dividend. If mNAV is above 1x, they can sell MSTR shares through the ATM. If mNAV drops below 1x, they can rely on the USD reserve (which currently covers more than two years of dividends). If the reserve were depleted, they could ultimately sell BTC derivatives or BTC from their treasury. With UST and Anchor, it was just “trust me bro, we’ll keep paying”.

A drop in price affects the two systems very differently. When UST lost its peg, confidence collapsed and the market quickly assumed the system could go to zero. With STRC, a lower price mechanically implies a higher effective yield, which can attract new buyers. For example, in a completely bearish scenario, if STRC were trading at $50 with a 12% dividend rate, the effective yield would be around 24%.

Finally, the time dynamics are completely different. Luna/UST was a fragile system that could collapse in a matter of days after a loss of confidence. In the case of STRC, even the worst-case scenario outlined earlier would unfold much more slowly (very slow death), potentially over several years, unless you assume a sudden and catastrophic collapse (-90%) in the price of BTC in just a few months.

TL;DR

STRC is a yield instrument backed by Strategy’s bitcoin treasury. Its dividend rate is dynamically adjusted to keep the price close to par ($100).

You can currently earn an 11.5% annual yield paid monthly on a mostly stable instrument, with very transparent risk.

STRC is essentially a way for Strategy to turn demand for yield into structural buying pressure for BTC.

The structure can scale massively without increasing MSTR’s leverage, as long as Strategy simultaneously runs ATMs on both STRC and MSTR (mNAV>1x required). This means Strategy could absorb $10bn (or much more) of new demand into STRC while keeping its leverage ratio stable at around 33% and its credit risk unchanged.

Every $1 of STRC issued should roughly translate into $3 of BTC added to the treasury, thanks to the common-stock ATM used to maintain the leverage ratio. Based on rough math, $100M of daily STRC volume at par ($100) can lead to $100M-$150M of BTC purchase.

Strategy effectively turns BTC exposure into two different tranches of risk: STRC holders receive a relatively stable yield with low volatility, while MSTR shareholders absorb the remaining upside and volatility of BTC. As Lavoisier famously put it: “Nothing is lost, nothing is created, everything is transformed.”

The whole structure is designed to increase bitcoin-per-share (bps) over time, which ultimately benefits MSTR common shareholders, because it means MSTR should mechanically outperform BTC.

Short-term drawdowns of 5-10% in STRC are possible, but as long as confidence in the structure remains intact, the market tends to arbitrage the price back toward par.

The real risk is not a sudden collapse but a prolonged BTC bear market, which could gradually stress the structure over time.

Even the (very unlikely) worst-case scenario would unfold slowly, thanks to the USD reserve and the flexibility Strategy has to adjust the dividend. If MSTR were to collapse, it would likely not happen in a spectacular and brutal way like Luna/UST, but rather through a slow and prolonged deterioration.

It makes very little sense to be bullish on BTC while being bearish on MSTR and STRC. Based on Strategy’s current level of risk (subject to change), MSTR can’t really die without BTC dying first.

I hope this article makes a few things clearer about STRC and the current MSTR playbook. If you have any questions or would like me to clarify something, feel free to comment below or ask me directly on Twitter!

ATM = “At-the-Market” program, allowing a company to issue and sell shares directly into the market at the prevailing price.

So I’m going to say ‘leverage’ even if I’m referring to the amplification ratio.

In practice, prices would obviously be affected, but given that the company’s stock price and BTC price are highly correlated, it’s a reasonable simplifying assumption

The STRC mechanics are elegant but underappreciated. What's interesting is how this converts fixed-income yield-seekers — traditionally the most Bitcoin-averse investor class — into indirect BTC accumulators. The feedback loop is compelling: more STRC issuance → more BTC buying → higher BTC price → higher NAV premium → more STRC demand. The real risk, as you note, is whether the premium holds when sentiment turns. In 2022, MSTR's premium collapsed to a steep discount, which broke the flywheel. I'd be curious whether the improved institutional liquidity around spot ETFs changes that dynamic in the next downturn.