The Microstrategy playbook : what most people get wrong

Strategy, risks, and common misconceptions

Welcome to this article about MicroStrategy, I am Viktor and you can find me here on Twitter and here on Telegram. Enjoy your reading !

NB: you can now become a paid subscriber to this newsletter to get access to paywalled articles as well as all the future resources I’m planning to share.

I’ve been seeing a lot of takes about (Micro)Strategy and many of them show a lack of understanding of this company and how it operates. In this article, I will try to explain a few important things to clarify the MSTR playbook. I have structured it with a series of questions and answers.

Why can’t MicroStrategy be considered as a ‘worse version of a BTC ETF’ ?

MicroStrategy holds bitcoin on its balance sheet, so it is definitely a proxy for $BTC, but the big difference compared to a BTC ETF, is that Microstrategy is trying to increase the BTC holdings / share as time goes by.

When you buy a share of IBIT (BlackRock BTC ETF), you know that it will always correspond to a fixed amount of BTC, whereas when you buy a share of MSTR, you are hoping that this share will accrue value in BTC terms over time.

What is the Microstrategy premium and why doesn’t it compress to 1 ?

The Microstrategy premium to NAV (Net Asset Value) is the ratio between the market cap of Microstrategy and their bitcoin holdings : many people expected the MSTR premium to collapse once the BTC ETFs were approved because ‘why would people buy a worse vehicle to hold bitcoin’ ? Well obviously that’s not what happened at all, and the premium actually grew a few months after the launch of the ETFs.

And the reason is exactly stated in the answer to the previous question : unlike ETFs, MicroStrategy is trying to increase the BTC holdings / share, so when you buy MSTR shares, you are (theoretically !) buying both the current BTC / share as well as the potential additional BTC / share that will be bought in the future. If you consider that Microstrategy will only continue to buy more BTC, you then realize that there should be a ‘floor’ on the MSTR premium that is above 1.

But of course, if you think that they could be forced to sell their BTC at some point in time and reduce the BTC/share as a consequence, then the premium could very well become a discount.

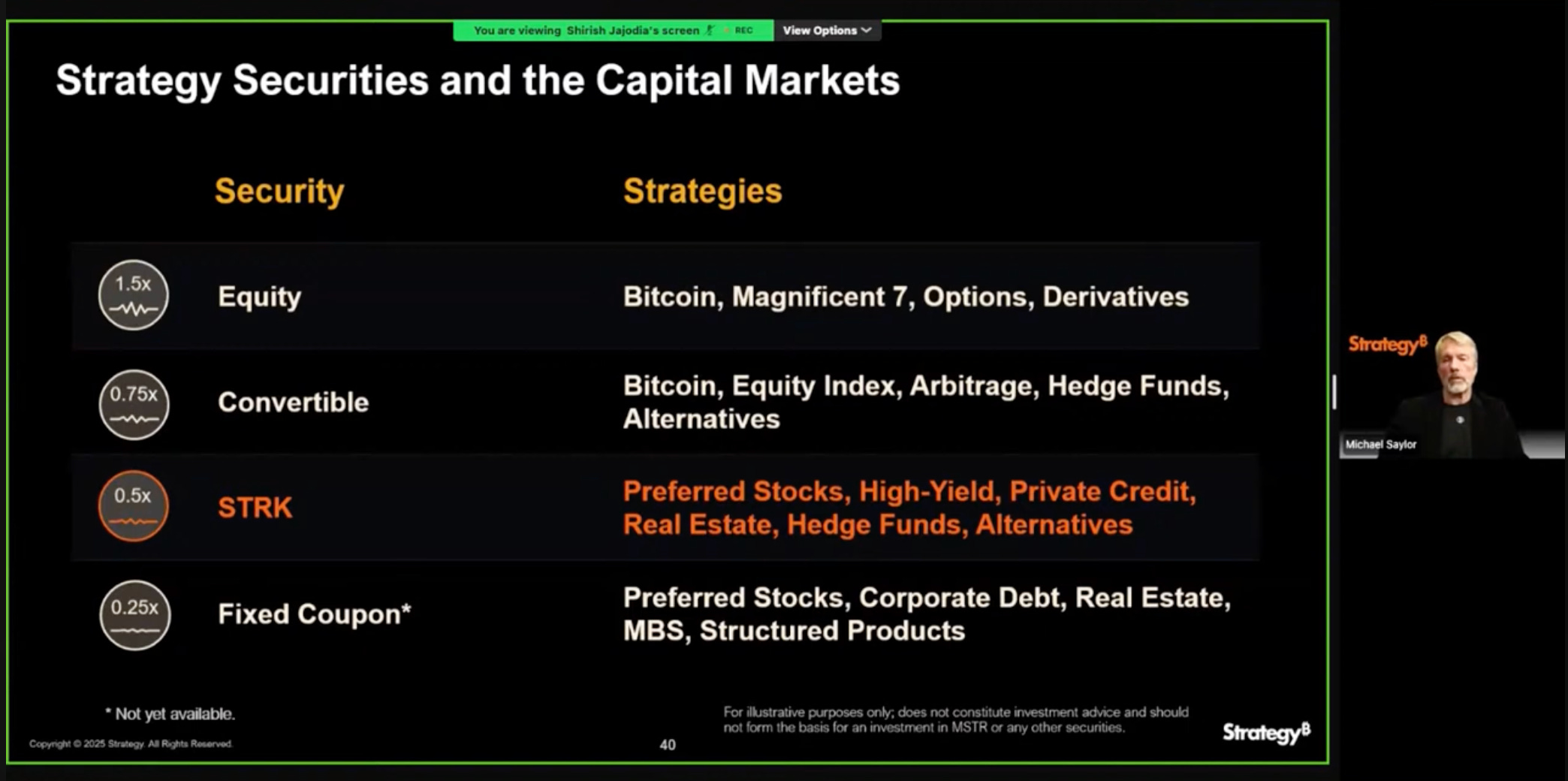

What exactly is the Microstrategy playbook ?

This slide shows how you should understand MicroStrategy's business :

They take the [high returns + high volatility] provided by Bitcoin (input)

And they offer a wide range of securities (fueled by this 'BTC engine') to the capital markets (output).

The MSTR stock is supposed to trade in a similar way as 1.5x-2x levered BTC, ie higher returns and higher volatility than BTC, while on the same time Saylor can provide other products that will have lower returns and lower volatility as BTC, such as the convertible bonds or the preferred stocks STRK. (In some way, the MSTR stock takes the additional upside AND downside volatility that is stripped away from the lower risk fixed income products)

This whole MSTR machinery basically generates a "permanent" flow of capital into BTC coming from people that don't want to outright buy BTC but are interested in the return/yield profile of the lower risk securities offered by MSTR. (At least this continues as long as the demand for these products have not dried up.)

How long can this playbook keep working ?

The whole strategy heavily relies on :

BTC having both high returns and high volatility

MSTR having high volatility

People buying MSTR at a premium to NAV

Of course, these conditions are somewhat intertwined. The return+volatility profile of bitcoin is the first condition that basically feeds the whole engine. Then, the high volatility of MSTR enables Saylor to attract convertible bond traders, and also to sell these convertible bonds at a higher premium (the higher the premium the better for MicroStrategy). Finally, the MSTR premium remaining elevated enables Saylor to both sell the convertible bonds at higher premium and to increase the BTC/share by simply selling shares for buying BTC.

The average BTC purchase price for MSTR keeps going up. Isn’t there a risk when the cost basis goes too high ?

This is a very prominent misconception people have about MSTR, so let me state this very clearly: The BTC cost basis of MicroStrategy is an absolutely irrelevant metric !

Here is what Saylor has done since November : he has bought $21bn worth of BTC at a price going from $76k to $107k, which has tremendously increased the average purchase price of the BTC owned by MSTR… while also reducing the overall leverage of the Microstrategy company !

How is that possible ? Among the $21bn he used to buy BTC, $17bn of these funds come from what we call the ATM = ‘at-the-money offerings’, which basically refers to the fact of issuing new MSTR shares and selling them on the market.

Let’s imagine a company that is worth $100bn in valuation, that has $10bn in debt, and that holds $50bn of $BTC. The ‘leverage ratio’ of the company with regards to BTC is $10bn / $50bn = 0.20.

Now if the company issues $10bn worth of new shares, and immediately buys $10bn worth of BTC with the proceeds, what happens ? The new valuation of the company is $110bn, while the $BTC holdings are $60bn and the debt did not change. Now the leverage ratio is $10bn / $60bn = 0.1666. The leverage ratio went DOWN while the average purchase price could have very well gone up in the meantime… but this average cost basis is completely irrelevant.

Note also that the number of shares have increased by 10% while the amount of BTC has increased by 20%, which means that the BTC holdings / share has gone up with this operation.

I rounded up the numbers to make the maths easier, but these numbers I just used are not too far from the reality of MSTR. The BTC cost basis of MSTR could very well go up while the overall risk and leverage involved could decrease in the same time.

Why does Saylor always buy the top, why does his weekly average purchase price look so high each week, and why does he not try to time the market and buy dips ?

Think about the ATM mechanic I just described in the previous answer : what mostly happened from November to February is that Saylor sold MSTR to buy BTC. And MSTR is very correlated to BTC. Which means that he is buying BTC by selling an asset that moves almost exactly like BTC.

So the notion of ‘buying at a high USD price’ is completely irrelevant : if he buys BTC at a high average price, it also means that he just sold MSTR at a similar ‘high average price’, and vice-versa. Buying ‘BTC at a cheap price’ in this situation means ‘buying BTC when the MSTR/BTC ratio is high’, while the BTCUSD price is close to irrelevant.

This also explains why he does not try to buy dips : buying dips on BTC would mean selling dips on MSTR at the same time. He obviously won’t focus on putting the selling pressure on his stock exactly when the stock is weak, he would rather do it when the stock is strong.

Could he try to time the market by selling MSTR shares at a ‘good USD price’ and then wait to buy BTC on a dip ? Yes, he could, but that’s called timing the market, and he does not pretend to have an edge on that matter. Timing the market could very well mean being forced to buy BTC at a worse price, so his goal is not to do that.

How levered is MicroStrategy ? Can Saylor blow up ?

Once again, the leverage of MicroStrategy is a topic that everyone seems to be freaking about while they usually don’t know a single thing about it.

The current debt of MicroStrategy is around $7.2bn, and at the time of writing, they hold around $46bn worth of $BTC. Note that given the nature of the debt (mostly convertible), a lot of this debt will simply be converted into equity, so they won’t even have to repay the debt (most of that debt is already way higher than the strike price of the convertible bonds).

But let’s assume anyway that it’s the debt that they will have to repay in dollars. $7.2bn/$46bn corresponds to a leverage of less than 16%. This means that (given the current numbers!) the price of BTC should go as low as $15.1k for the BTC holdings to be equal to the debt amount.

Does this mean that MicroStrategy does have a liquidation price of around $15k ? Even that is absolutely not correct : as you can see on the table above, they have to repay the debt over several years, and the first payment is… $1.01bn in 2028. Then $3bn in 2029. Then $800M in 2030. Then $604M in 2031. Then $800M in 2032.

Basically for MicroStrategy to be in trouble, we would need $BTC to trade below $15k from 2028 to 2032. Sounds quite unrealistic, right ? If this does not sound unrealistic to you, I don’t know what kind of future you imagine for BTC, but that would definitely be a failure of bitcoin to me.

Does Saylor have a liquidation price ?

Microstrategy does not have a liquidation price, and cannot be “hunted”. To ‘hunt’ Microstrategy based on current ratios, you should both have BTC trading at a very low price AND stay there for a prolonged time, so it’s very clear that this has nothing to do with your usual leverage position that gets instantly liquidated at a certain price.

Now, let me add that Saylor has recently stated in their earnings call that they are targeting a ‘leverage ratio’ of 20%-30%, which is higher than the current leverage ratio (16%). So they are very probably going to ‘lever up’ the structure again in the coming weeks, by selling both new convertible bonds and preferred stocks. This means that the $15k ‘danger price’ will also go up. (Note that this ‘danger price’ has nothing to do with the BTC cost basis of MSTR, it can go down while the cost basis goes up…).

I hope this article makes a few things clearer about the MicroStrategy playbook. If you have any questions or would like me to clarify something, feel free to comment below or ask me directly on Twitter.

Thank you for reading this article,

Cheers,

Viktor.

Ref link shill : My favorite exchange is Bybit, it is where I take most of my perp trades. If you want to start trading there, you can use my referral link by clicking here or use my code AOZDLZ6

This was a nice read, definitely cleared up a few things I haven't fully grapsed before regarding Mr. Saylor's endevours

Just remember all caps, when you spell the man's name