The MSTR Preferred Share Playbook

Why Saylor is replacing converts with perpetual prefs

Welcome to this article about MicroStrategy, I am Viktor and you can find me here on Twitter and here on Telegram. Enjoy your reading !

I haven’t written an article focused on MSTR in a long time. Four months ago, I wrote an article on the general framework around BTC treasury companies and why it can make sense buying them at a premium, and in February 2024, I wrote a presentation of the MSTR playbook and the common misconceptions regarding this company. Since then, Saylor has pivoted away from convertible bonds as the main source of leverage, and is now entirely focused on preferred shares. So it’s time for an update.

This article will simply be an introduction to these MSTR preferred shares, because most people aren’t familiar with them at all and tend to view them as the “new Ponzi toys invented by Saylor out of desperation to keep raising funds.” (No problem with holding that opinion, as long as you actually understand how they work!)

Preferred shares are a hybrid structure: they are technically equity, but they behave much more like debt instruments than like ordinary common stock. All the preferred shares issued by MicroStrategy so far are perpetual preferreds, which means they never “come due” and never have to be repaid, unlike bonds.

The gist of the strategy for Saylor is this: issue preferred shares that pay roughly a 10% annual yield to holders (in perpetuity!), use the proceeds to buy BTC, collateralize the preferreds with the BTC stack, and then rinse and repeat ad infinitum so that MicroStrategy is perpetually levered long BTC. Why is this supposed to work? Because Saylor and MSTR shareholders expect BTC to deliver returns far greater than 10% per year. So issuing “debt-like” instruments at ~10% to buy an asset that compounds at 20–30% annually should, over the long run, outperform the underlying asset itself.

Disclaimer: This is absolutely NOT financial advice. I’m not recommending buying or selling MSTR or its preferred shares. This article is for informational purposes only.

Breakdown of the MSTR Preferred Share Series

$STRF: Long Duration Senior Credit

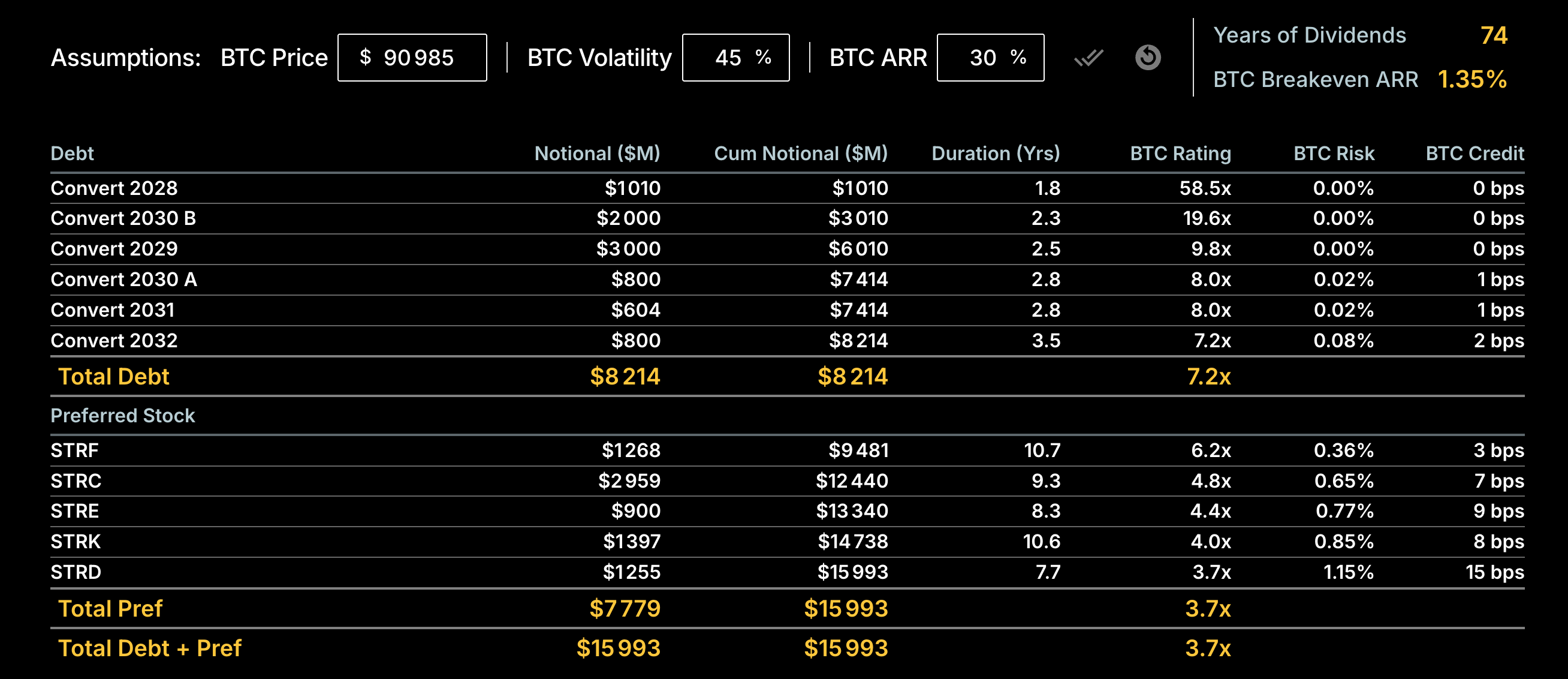

$STRF, “Strife”, is the most simple preferred share: Its annual dividend is $10, it sits on top of the capital stack (so it is senior to all the other prefs, but not the convertible bonds), and the dividends are cumulative (this means that the dividends would have to be paid later on even if they were to be suspended for some time).

The price can move up and down depending on market demand, so that the actual “interest rate” you get on the instrument is set by market demand. For example, when $STRF is trading at $110, you are getting a 9.1% effective yield, and when it’s trading at $90, you are getting an 11.1% effective yield.

$STRF is the “safest” preferred because it’s senior to every other pref, it’s the most collateralized, the goal of Saylor is to make it an “investment grade” like product.

The current “BTC Rating” (or collateralization ratio) of $STRF is 6.2x. This means the value of the BTC stack is 6.2 times larger than the combined value of all convertible bonds + STRF, which are the most senior instruments in the capital structure in the event of a liquidation.

$STRD: Long Duration High Yield Credit

$STRD, “Stride”, is very similar to $STRF as it also distributes an annual divided of $10, but it sits at the bottom of the capital stack. So it’s the most junior pref, (but it’s senior to the common stock), and its dividends are also non-cumulative. This means that Strategy could decide to suspend the dividend payments without having a “penalty” (but the price of STRD would obviously take a meaningful hit if that were to happen). $STRD is basically the junk bond of the “yield curve” created by Strategy.

The current price of $STRD is $72, which means the effective yield on $STRD is currently 13.3%.

The current “BTC Rating” (or collateralization ratio) of $STRD is 3.7x. This means the value of the BTC stack is 3.7 times larger than the combined value of all convertible bonds + all prefs senior to STRD + STRD.

$STRK: Structured Bitcoin

$STRK, “Strike”, is the preferred share version of a convertible bond. It pays an annual dividend like the other prefs, and this dividend is $8 per year, but $STRK is also convertible. 10 shares of $STRK can be converted into 1 share of $MSTR. $STRK is junior to all prefs except $STRD. The dividends of STRK are cumulative.

The current price of $STRK is $82, so the effective yield is 10.1%. $MSTR price is currently $176 so 1/10 of $MSTR is $17.6, 82-17.6=64.4 and 8/64.4 = 12.4, so the “cash-on-cash yield” of STRK is 12.4%.

It is called “structured bitcoin” because you get some of the upside of BTC, but with way less downside, and a dividend payment on top.

$STRC: Short Duration High Yield Credit

$STRC, “Stretch”, is the most novel structure for a preferred share, it is basically a stablecoin with a “soft peg” at $100, which pays a variable yield monthly.

The current dividend yield is $10.5 a year, but it can get adjusted up or down every month. If the price of $STRC is below $99 at the end of the month, Strategy will increase the dividend rate until it goes back to “peg”, and if the price of $STRC goes above $100 (or $101), Strategy will usually issue and sell more $STRC. They also have the option to call $STRC at $101, which provides a ceiling above which it makes no sense for buyers to buy more $STRC. The dividends of $STRC are cumulative too.

As you can see, $STRC has barely been trading at par so far, and it is at risk of a deeper depeg when the market is fearful. One reason for that is that the dividend rate gets adjusted “too slowly” compared to the speed at which BTC price can meaningfully go down. I don’t want to expand my thoughts much further on STRC because that would probably be the topic of another article, but it’s an extremely interesting product to track, in my opinion.

$STRE: “Euro STRF equivalent”

$STRE, “Stream”, is the euro equivalent of $STRF, it is denominated in euros and pays 10€ worth of dividend a year. It is junior to $STRF and $STRC, but senior to $STRK and $STRD. There is not much more to say about $STRE, we don’t have any price history yet as it’s just been launched.

What are the advantages of preferred shares vs bonds?

Before turning to preferred shares, Saylor’s main way to take on leverage was to issue convertible bonds. They worked very well, but they essentially require two things to remain accretive: a premium to mNAV (the higher, the better) and high implied volatility on MSTR. Both BTC volatility and MSTR volatility have fallen significantly over the past year, making convert issuance less attractive. This means Saylor had to find a new instrument to implement “intelligent leverage.” But I’d argue that preferred shares aren’t just a stopgap, they are actually superior to convertible bonds. Saylor seems to agree, since Strategy has announced its intention to focus exclusively on preferreds going forward and retire all outstanding converts over time.

Here are the main advantages of preferreds over convertible bonds, and over bonds in general:

There is no default risk on preferred shares. They are equity, not credit. If dividends are suspended, it is not considered a default, unlike missing an interest payment on a bond.

Perpetual preferreds have no refinancing or repayment event, because they never come due. By contrast, any bond introduces refinancing/rollover risk, which can occur at the worst possible moment, for example, in the middle of a bear market when issuing new debt is expensive or impossible. With preferreds, Strategy can pay dividends in a slow drip over time instead of facing a single large lump-sum repayment. This makes the structure far safer and far more flexible: there is no cliff risk, no maturity wall, and no need to raise a massive amount of capital at a potentially terrible moment.

Preferred shares simplify the credit stack, because everything becomes homogeneous. Instead of a dozen bonds with different terms and maturities, you end up with one perpetual preferred for each risk bucket: long-duration senior credit (STRF), long-duration high-yield credit (STRD), short-duration high-yield credit (STRC), and “structured bitcoin” (STRK). It may not look simple at first glance, but it is, and each preferred can become a well-defined product that investors recognize and understand.

All of these instruments trade on public markets, which makes them liquid (and thus priced at a liquidity premium relative to private instruments) and accessible to a far larger pool of capital. Anyone can buy MSTR preferreds and provide leverage to Strategy, unlike convertibles, which rely on a relatively small group of institutional buyers.

The fundraising process with preferreds is extremely efficient. Issuance is automated through an ATM program, costs almost nothing compared to issuing a new bond, and scales “infinitely” (subject to market demand). Yes, there are IPO-level costs when a new preferred series is launched, but once that hurdle is cleared, raising capital becomes very cheap.

“But Strategy had 0% interest debt before the prefs, and now they are paying 10% a year, Saylor is getting increasingly desperate!”

This is a very common misconception about the preferreds. People assume that the 0% convertible bonds were truly zero-interest debt, without realizing that these instruments had obvious hidden costs: the equity they converted into. Those convertible bonds were absolutely not zero-cost once you take into account the dilution required to “repay” the debt via newly issued shares.

With preferred shares, instead of having to issue one huge block of stock all at once (as with converts), Strategy simply issues and sells a small amount of new MSTR shares every month or every quarter. Some people think this introduces a major new risk, but preferred issuance is actually more accretive for MSTR shareholders than convertible bonds, especially in terms of BTC per share. I don’t have time here to walk through the full math, but if you run the numbers yourself, you’ll see that preferreds offer more leverage than convertibles, and therefore generate more long-term shareholder value (assuming BTC continues to deliver a reasonably high CAGR, of course).

I highly recommend watching the MicroStrategy Q1 2025 earnings call if you’re interested in this specific point:

“But how will Strategy pay the yield?”

This is probably the most common concern regarding the preferred shares. The answer is very simple: the yield will be paid by issuing and selling new shares of $MSTR. That’s the entire business model. As long as mNAV stays above 1x, Saylor will continue paying dividends by selling new shares; he is not looking for any other source of revenue to fund them.

Note that the mNAV figure Saylor is likely to rely on is the fully diluted mNAV shown on the Strategy website — the ratio of enterprise value (market cap + debt + preferreds) to the company’s BTC holdings. At the moment, this fully diluted mNAV is still around 1.12x, while the undiluted mNAV (market cap / BTC) sits closer to 0.85x.

What if mNAV drops below 1x? Saylor recently addressed that question in a recent conference: https://x.com/Oliverderci1/status/1968504994572759089

One very important thing to keep in mind is the scale of the annual dividend payments: they currently total around $700M per year, while the average daily trading volume of $MSTR is between $3–4B. This means that funding the dividends by issuing new MSTR shares has a negligible impact on the stock in terms of sell pressure.

“Is there a death spiral scenario for MSTR that could collapse the price of BTC?”

Let’s restate the key point from the previous section: Strategy needs to find about $700M per year to pay the dividends. Suppose, for the sake of argument, that they chose to sell BTC to fund them. That would create $700M of additional annual sell pressure on BTC.

$700M per year.

That is completely negligible in terms of order-book impact.

That said, BTC sales would be an absolute last resort for Strategy. If they end up selling BTC, it would almost certainly be because BTC is already in a difficult environment. In a severely bearish scenario, yes, MSTR could be selling BTC at depressed prices, but it is absurd to think that these sales would meaningfully cause BTC to go down.

To put things in perspective: $700M is roughly one good day of BTC ETF inflows. Spread over a full year, it’s essentially nothing.

Conclusion

I don’t want this article to become too long, so I’ll leave a deeper discussion of the preferred shares for another piece. For example, I haven’t really addressed the risks for pref holders, the pricing dynamics of these instruments, or their recent price action.

My view is that the preferred shares are currently undervalued, and that the market is overestimating their risks. But I also understand that they could stay undervalued for some time, and even become “more undervalued”. Ultimately, it all comes down to the market’s trust in BTC’s long-term performance and in Saylor’s decision-making. It’s easy to see why there’s such a wide range of opinions on that subject.

I’m also not claiming that MSTR or its preferred shares are risk-free. BTC itself is a risky asset, so a structure that is levered long BTC is, by definition, even riskier. The purpose of this article was simply to make people more familiar with these instruments, which can look complex at first glance but are actually fairly intuitive once you understand the mechanics.

Thank you for reading this article,

Cheers,

Viktor.